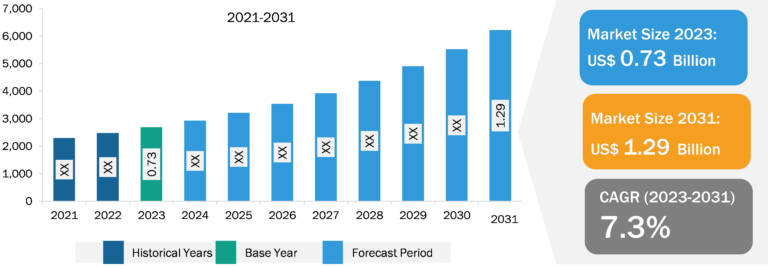

Osteoporosis treatment Market

The osteoporosis treatment market includes various drugs and therapeutic modalities carefully developed to combat osteoporosis—a disease characterized by the bones becoming brittle and prone to fractures. The therapeutic arsenal often includes bisphosphonates, hormone therapy, denosumab, and a range of nutritional supplements recommended along with lifestyle adjustments such as increased physical activity and a calcium-rich diet. The market is driven by the growing elderly population and increasing recognition of osteoporosis as a pressing health issue. Relentless research and development efforts aim to introduce breakthroughs and more effective interventions to treat this debilitating disease.

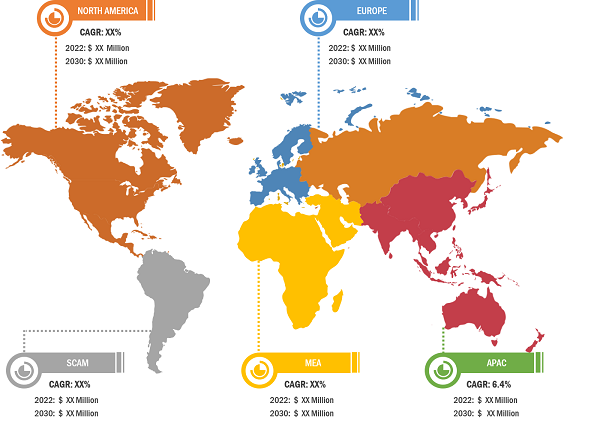

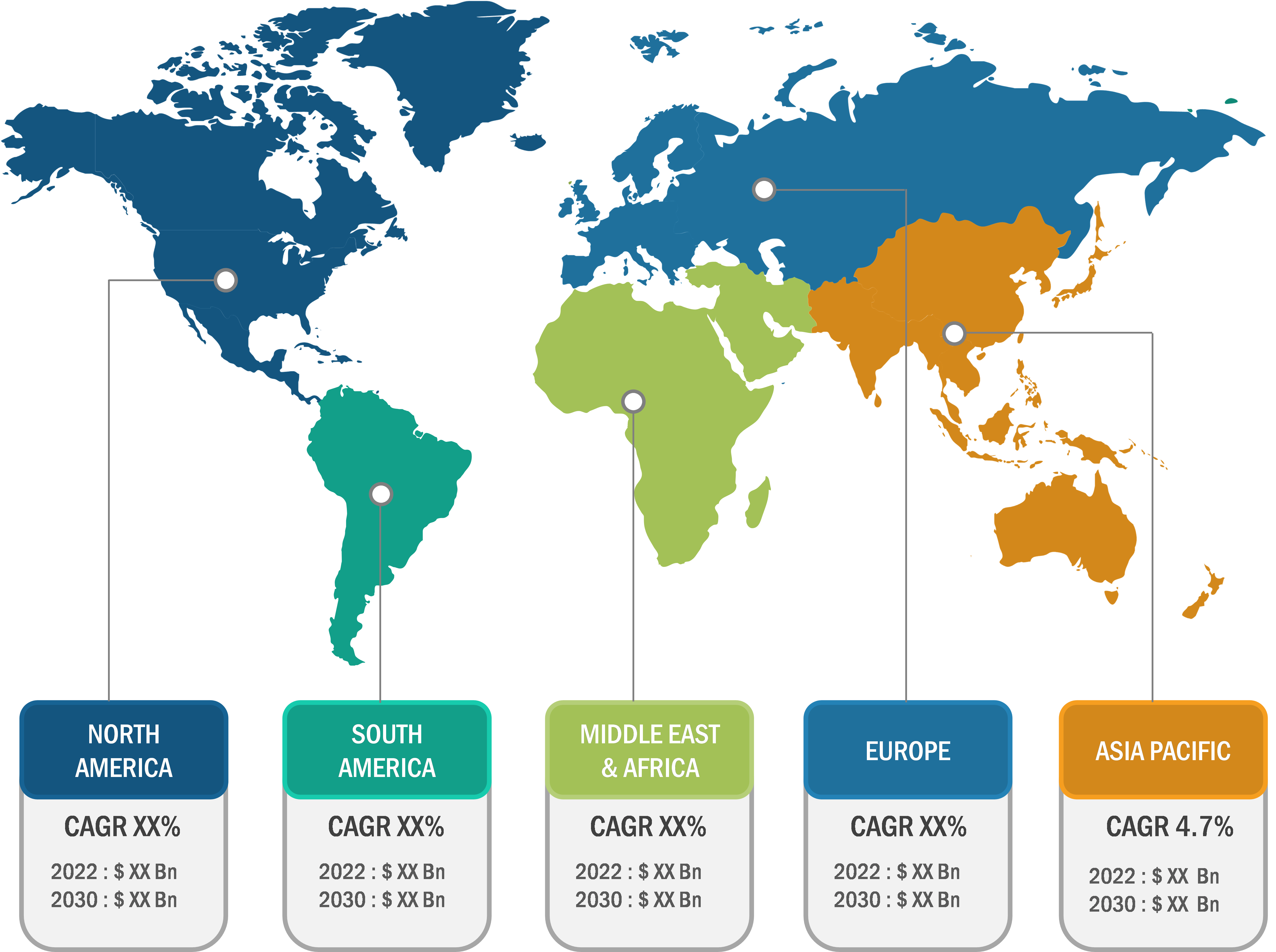

The market in North America was valued at US$ 8.26 billion in 2023 and is projected to reach US$ 11.26 billion by 2031; it is expected to register a CAGR of 3.9% during 2023–2031. This is due to the aging population in the region with greater awareness of osteoporosis, advanced healthcare infrastructure, and comprehensive access to medical services enable timely diagnosis and treatment. In addition, the presence of large pharmaceutical companies and ongoing research and development initiatives are encouraging the introduction of innovative therapies. Lastly, favorable reimbursement policies and insurance coverage support patients seeking osteoporosis treatment support the market growth in North America.

The Asia Pacific osteoporosis treatment market is expected to record the fastest CAGR during 2023–2031. The region is characterized by a rapidly aging population, particularly in countries such as Japan and China, leading to an increased prevalence of osteoporosis. Increasing health awareness contributes to higher diagnosis rates. The growing middle class and increased accessibility to healthcare are driving demand for osteoporosis treatments. Additionally, improvements in healthcare infrastructure and the emerging pharmaceutical sector make Asia Pacific a hub for the growth of the osteoporosis treatment market.

Growing Digital Health Solutions to Provide Market Opportunities

Digital health solutions provide a platform for more holistic and patient-centered care, enabling healthcare providers to monitor bone health and medication adherence remotely. These solutions include telemedicine, wearable devices, and remote monitoring. Digital health solutions increase patient engagement, facilitate real-time monitoring, and improve adherence to treatment plans. Timely reminders to patients, provision of educational resources, and streamlined communication with healthcare professionals together help in improving treatment plan adherence. Telemedicine facilitates access to specialized care, especially in undeveloped areas, thereby broadening osteoporosis treatment horizons.

The Fracture Risk Assessment Tool App (FRAX App), developed by the Center for Metabolic Bone Diseases at the University of Sheffield, UK, is a user-friendly app for calculating an individual patient’s 10-year probability of a major osteoporotic event (clinical spinal, forearm, hip or shoulder fracture) and probability of osteoporotic hip fracture by entering simple clinical and demographic details. For clinicians, the app offers PIN protection for saving assessments, patient results management features (save, delete, and sort options), and email-sharing functionality for patient assessments (responses and results). My Osteoporosis Journey is an app for women newly diagnosed with asymptomatic osteoporosis. The app aims to support patients with treatment through decision-making and self-management and is used as a complement to primary and secondary healthcare workers. The app also helps reduce anxiety and give patients more confidence and a sense of security. The Hip Fracture Risk Calculator app calculates the risk of hip fracture and in-hospital mortality after a hip fracture based on patient demographics and comorbidities. My Osteoporosis Manager @Point of Care is a management tool that allows patients with osteoporosis to track and store relevant health information between doctor visits. It includes the ability to record detailed health information in a digital journal, manage medications and treatments, track bone-specific symptoms and side effects, easy-to-understand charts that record test results and medication adherence, access to patient education materials, and share information with the patient’s healthcare provider.

The development and implementation of digital technologies is increasing rapidly. Healthcare departments are committed to collaborating with academics, industry, and the commercial sector to deliver trusted digital solutions that improve patient care. Digital health tools that include reminders, risk assessment, or education can reduce secondary fracture rates, improve bone mineral density testing, and initiate osteoporosis therapy. Leveraging these digital tools improves patient outcomes and opens up innovative opportunities for creating data-driven, personalized treatment strategies and developing integrated care models in the osteoporosis treatment market.

Growing Awareness and Diagnosis of Osteoporosis to Drive the Market Growth

Awareness about osteoporosis has increased significantly among both health professionals and the general public. Initiatives by health organizations and pharmaceutical companies play an important role in educating people about osteoporosis and its early detection, prevention, and available treatment options. As a result, more people are being diagnosed with osteoporosis, increasing the demand for osteoporosis treatment.

World Osteoporosis Day, a global health event, is celebrated on October 20 and promotes early diagnosis of the disease, its treatment, and ways to prevent it. Each year, this campaign encourages people to take preventive measures and care for their bone health to avoid the risk of osteoporosis and many related complications. In April 2022, the International Osteoporosis Foundation announced #LiftOffForBoneHealth, an exciting new online public awareness campaign in collaboration with the European Space Agency (ESA). The campaign championed bone health by encouraging people worldwide to regularly engage in weight-bearing and resistance exercises to help them build and maintain strong bones throughout their lives.

With the help of genetic testing and data analysis advances, healthcare providers can identify high-risk osteoporosis patients and tailor treatment plans accordingly. Osteoporosis can be diagnosed with the help of a simple X-ray test called a DEXA scan. The scan is quick, painless, and easy to perform. Women over 65 and men over 70 should be examined. On the other hand, general blood and urine tests provide information about the general health status and the presence of elements that cause secondary osteoporosis. These markers are useful tools for identifying metabolic bone diseases because they provide information that cannot be obtained directly using bone densitometry or bone histomorphometry. Another commonly used marker test is bone turnover markers, which can measure amino- and carboxy-terminal peptides in bone matrix formation or degradation processes. Further, increasing demand for personalized medicine is also expected to drive the osteoporosis treatment market in the coming years.

Osteoporosis Treatment Market: Drug Class Overview

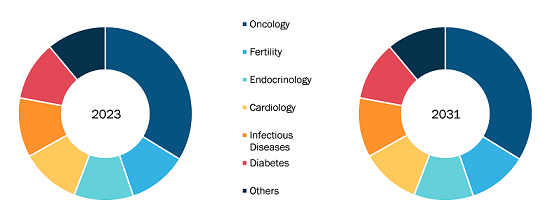

Based on drug class, the osteoporosis treatment market is divided into RANKL, bisphosphonates, selective estrogen receptor modulators (SERM), hormone therapies, and others. The RANKL segment held the largest market share in 2023. However, the hormone therapies segment is likely to register the highest CAGR during 2023–2031. Bisphosphonates segment also holds a considerable share in the osteoporosis treatment market. Bisphosphonates, which include compounds such as alendronate and zoledronic acid, are well-known for their effectiveness owing to the presence of active ingredients that inhibit bone resorption and increase bone density, thereby minimizing the risk of fractures. Furthermore, their cost-effectiveness and comprehensive insurance coverage contribute to their increased adoption in osteoporosis treatment.

In terms of type, the osteoporosis treatment market is segmented into primary osteoporosis and secondary osteoporosis. The primary osteoporosis segment held a larger market share in 2023 and is estimated to record a faster CAGR during 2023–2031. Primary osteoporosis occurs with aging, which results in slow bone renewal. Primary osteoporosis includes idiopathic osteoporosis, which occurs in children and young adults with unknown etiopathogenesis. Secondary osteoporosis occurs due to secondary factors such as an underlying health condition (gastrointestinal diseases, rheumatological diseases, and chronic kidney diseases) or certain medications (prednisone, hydrocortisone, and dexamethasone). According to a study published in MDPI titled “Osteoporosis: Molecular Pathology, Diagnostics, and Therapeutics,” secondary osteoporosis accounts for less than 5% of all osteoporosis cases and results from disease or medication use.

Osteoporosis Treatment Market: Competitive Landscape and Key Developments

Pfizer Inc.; Amgen Inc.; Cadila Pharmaceuticals; Eli Lilly and Company; Daiichi Sankyo Company, Limited; Teva Pharmaceuticals Inc.; Asahi Kasei Corporation; Novartis AG; Chugai Pharmaceutical Co., Ltd.; and Teijin Pharma Limited are among the key companies operating in the osteoporosis treatment market.