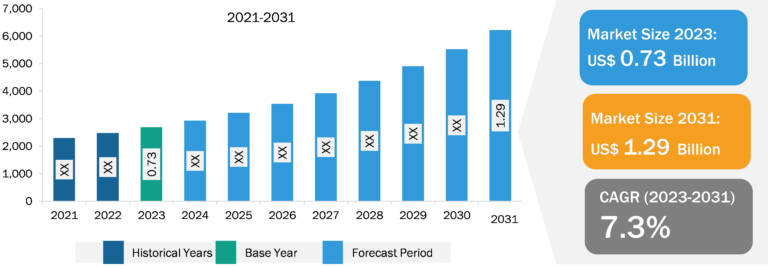

SOC as a Service Market

Various SMEs worldwide have been facing a rise in cyberattacks in recent years. According to Accenture’s Cybercrime study, small enterprises record 43% of total cyberattacks annually, of which 46% occurred in small businesses with 1,000 or fewer employees. As a result, on average, SMEs lose US$ 25,000 due to cyberattacks. In addition, in 2020, small enterprises faced over 700,000 attacks, which caused a total of US$ 2.8 billion in damages. Also, as per the World Economic Forum, ~95% of these attacks can be attributed to human error. Also, according to the Check Point, 43% of data breaches are caused by insiders or company employees, considering all cases, whether on purpose or not. Due to such increasing data breach activities, various SMEs witnessed a sharp decline in repeat customers. IBM unveiled that ~50% of small businesses require more than 24 hours to recover from an attack, as over 51% of all small businesses could not access their website for 8–24 hours. Hence, these alarming statistics raise the need for SMEs to implement cybersecurity services to help secure their businesses.

Verizon’s 2021 SMB Data Breach Statistics show that SMEs spend between US$ 826 and US$ 653,587 on cybersecurity incidents. According to the same report, cybercrime is also expected to increase by 15%, with costs estimated to reach US$ 10.5 trillion by 2025. Hence, various SMEs are investing in managed security services such as SOCaaS to meet the ever-increasing regulatory and legal requirements. Also, as SOCaaS can provide SMEs with access to a virtual security operations center (SOC), which is responsible for monitoring as well as analyzing network traffic, providing real-time alerts to security teams, and identifying security threats, its adoption is expected to increase in SMEs, creating future opportunities for the growth of the SOC as a service market.

US Dominates SOC as a Service Market in North America

The demand for SOC as a service in the US is due to the growing number of tech-savvy enterprises that are willing to invest in artificial intelligence (AI) technology. For instance, according to Goldman Sachs data, in 2022, the US invested US$ 47.4 billion in AI technology, which encouraged manufacturers to develop AI-SOCs. The AI supports the SOC providers to track real-time activities of cyberattacks and provide faster and more accurate responses against cyberattacks. For example, an AI-powered SOC can help organizations identify potential threats and vulnerabilities more rapidly and accurately. AI automates the threat detection process and allows security analysts to focus on higher-level activities, such as threat hunting and incident response. Thus, due to its scalability and accuracy, the AI-based SOC as a service is expected to fuel the market during the forecast period.

Many key players in the US are partnering to bring integrated Zero Trust Security to devices, networks, and applications. For instance, in March 2022, Cloudflare Inc. partnered with CrowdStrike to deploy seamless Zero Trust protection from the network to the user’s device. Cloudflare Inc integrated its Zero Trust platform with CrowdStrike Falcon Zero Trust Assessment (ZTA) to provide its customers with simple, powerful controls and secure access to applications. This also helps customers to identify and mitigate threats and take corrective actions to protect their data.

SOC as a Service Market Segmental Overview:

Based on service type, the SOC as a service market is segmented into prevention service, detection service, and incident response service. The prevention service segment recorded the largest SOC as a service market share in 2022, whereas the detection service segment is anticipated to register the highest CAGR during the forecast period. Based on enterprise size, the SOC as a service market is divided into SMEs and large enterprises. The large enterprises segment recorded a larger SOC as a service market share in 2022, whereas the SMEs segment is likely to record a higher CAGR during the forecast period. Based on application, the SOC as a service market is segmented into network security, endpoint security, application security, and cloud security. The endpoint security segment recorded the largest share in the market in 2022, whereas cloud security is anticipated to register a higher CAGR during the forecast period. Based on industry, the SOC as a service market is segmented into BFSI, IT & telecom, manufacturing, retail, government & public sector, healthcare, and others. The BFSI segment registered the largest share of the SOC as a service market in 2022, whereas the healthcare segment is anticipated to record the highest CAGR during the forecast period.

SOC as a Service Market Analysis: Competitive Landscape and Key Developments

Fortinet Inc, Atos SE, NTT Data Corp, Verizon Communications Inc, Thales SA, AT&T Inc, Arctic Wolf Networks Inc, Cloudflare Inc, ESDS Software Solution Ltd, and ConnectWise LLC are among the key SOC as a service market players that are profiled in the report. Several other essential SOC as a service market players were also analyzed for a holistic view of the market and its ecosystem. The market report provides detailed market insights to help major players strategize their growth.

- In 2023, Fortinet, one of the global leaders in broad, integrated, and automated cybersecurity solutions, announced new security operations center (SOC) augmentation services designed to help strengthen an organization’s cyber resiliency and support short-staffed teams strained by the talent shortage. Also, as part of Fortinet’s leadership efforts to help remove the cyber skills gap, the Fortinet Training Institute has added initiatives across its programs to increase access to its industry-recognized training and certifications.

- In 2022, Thales created a new cyber security operations center (SOC) in Morocco, the sixth in its international network. This center will provide real-time protection against cyberattacks in the country and across the African continent as a whole.