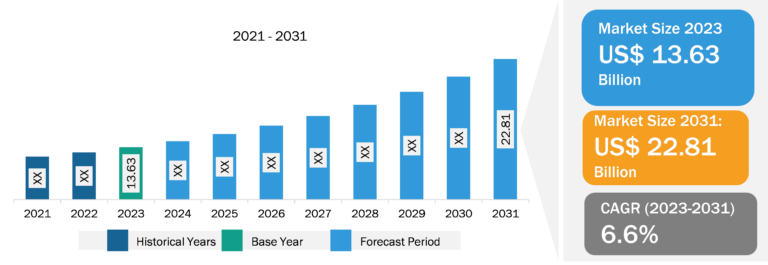

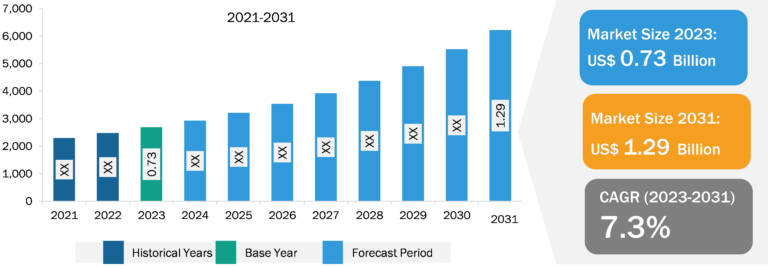

Spinal Implants Market

Factors such as the surging number of spinal implant procedures, and rising incidence of trauma and sport-related injuries propel the spinal implants market growth. However, the stringent regulations impede the growth of the market.

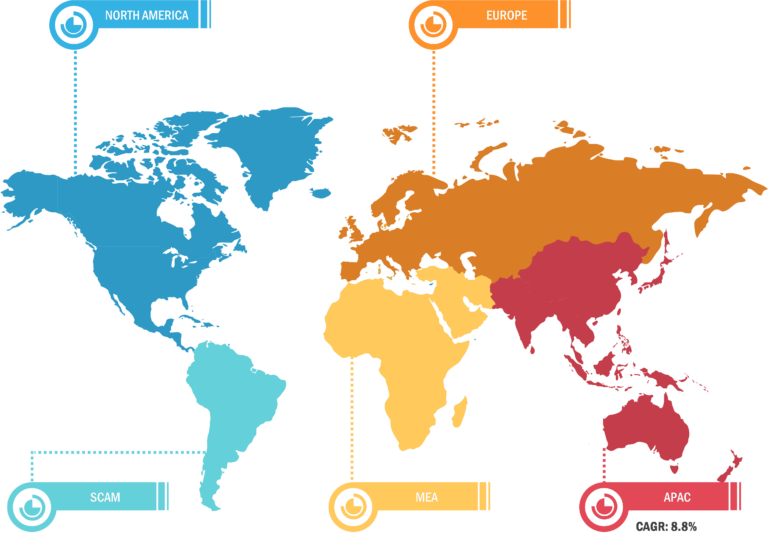

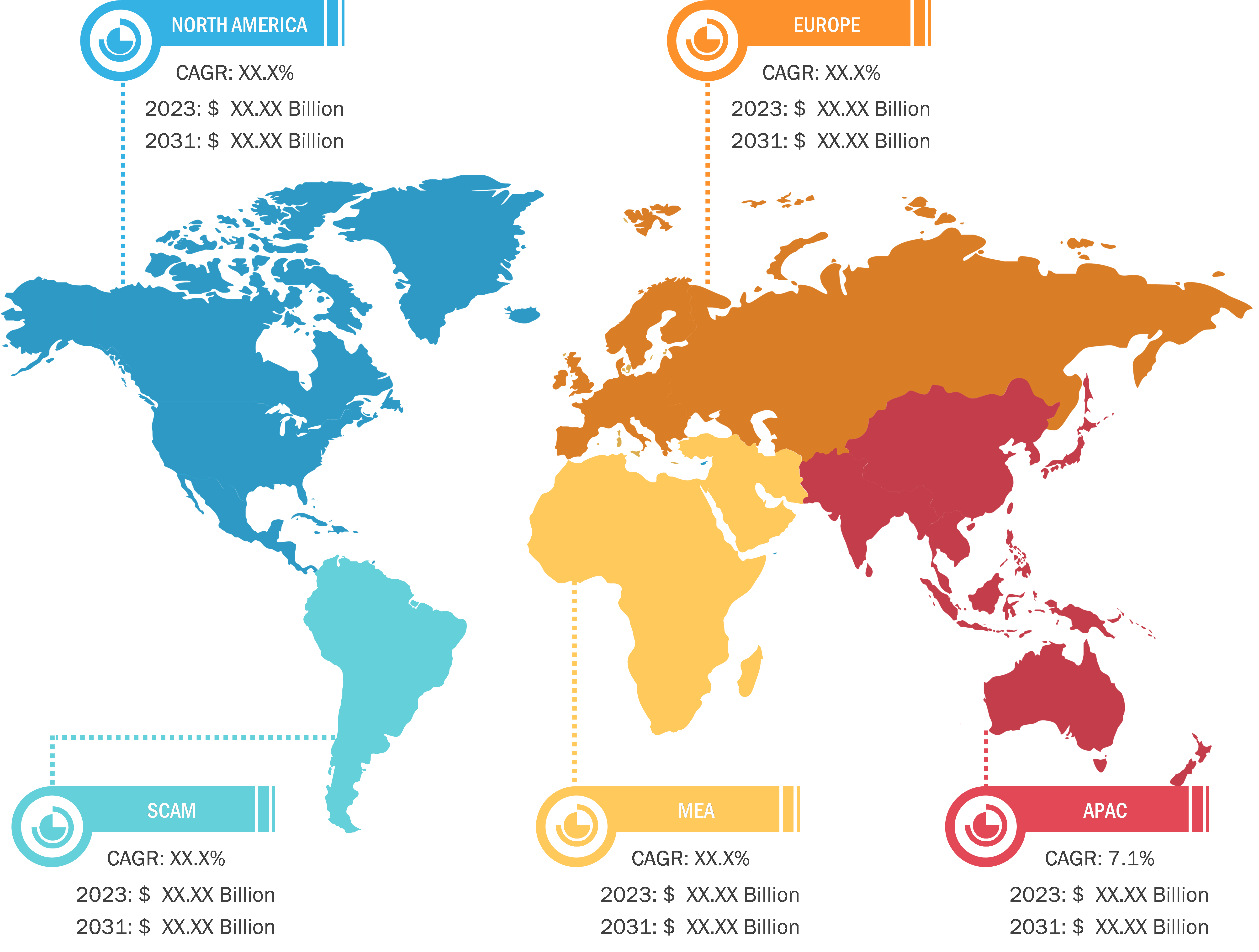

The spinal implants market in Asia Pacific is expected to grow at the highest CAGR during the forecast period. North America accounted for the largest share of the market in 2023. The growing adoption of the latest medical devices, the high prevalence of spinal injuries, and product innovations by key players contribute to the expansion of the spinal implants market size in North America. According to the Cleaveland Clinic, the US reports ~18,000 new traumatic spinal cord injury cases each year, which is equivalent to ~54 cases per 1 million population. Additionally, age-related wear-and-tear triggers the prevalence of lower back pain (LBP) among the geriatric population in the US, in turn, fuels the demand for spinal surgeries and implantable devices. According to National Health Services, in 2022, the lifetime incidence of LBP in the US is reported to be 60–90%, with an annual incidence of 5%. The source also states that 14.3% of new patients visit physicians each year because of LBP, and ~13 million people visit physicians due to chronic LBP. Thus, the high prevalence of spinal cord injury and LBP favors the spinal implants market progress.

Surging Number of Spinal Implant Procedures Drives Spinal Implants Market Growth

Spinal Implants Market: Segmental Overview

By product, the market is bifurcated into fusion spinal implants and non-fusion spinal implants. The fusion spinal implants segment held a larger market share in 2023. It is anticipated to register a higher CAGR during the forecast period. The market, by procedure, is categorized into foraminotomy, laminectomy, spinal disc replacement, spine fusion, and discectomy. The laminectomy segment held the largest market share in 2023; spine fusion is expected to register the highest CAGR during the forecast period. The spinal implants market, by material, is segmented into titanium, carbon fiber, and stainless steel. The stainless steel segment held the largest market share in 2023. The segment is anticipated to register the highest CAGR during the forecast period. The spinal implants market, by end user, is categorized into hospitals, diagnostic and imaging centers, and others. The hospitals segment held the largest spinal implants market share in 2023, and it is anticipated to register the highest CAGR during the forecast period.

The spinal implants market report, based on geography, is segmented into North America (US, Canada, and Mexico), Europe (Germany, France, Italy, UK, Russia, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, the UAE, the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Spinal Implants Market: Competitive Landscape and Key Developments

Stryker Corporation, Johnson & Johnson, Globus Medical Inc, ZimVie Inc, Camber Spine Technologies LLC, Spineart SA, Medtronic plc, Orthofix US LLC, ATEC Spine Inc, and B. Braun SE are among the prominent players profiled in the spinal implants market report. These companies adopt product innovation strategies to meet evolving customer demands, which allows them to maintain their brand name in the market.

A few of the recent developments in the spinal implants market, as per company press releases, are mentioned below:

• In October 2023, Silony Medical International AG completed the acquisition of Centinel Spine’s Global Fusion Business. Through this acquisition, Silony makes major entry into the US market & significantly strengthens its anterior standalone cage offering.

• In September 2023, Globus Medical Inc completed its merger with NuVasive Inc. The combined company provides surgeons and patients with one of the most complete musculoskeletal procedural solutions, enabling technological advances across the care continuum.

• In November 2022, NuVasive Inc. announced the commercial launch of the NuVasive Tube System (NTS) and Excavation Micro, a revolutionary minimally invasive surgery (MIS) technology offering complete solutions for transforaminal lumbar interbody fusion (TLIF) and decompression. With additions to the NuVasive P360 portfolio, the company enhanced its access and instrumentation technology capabilities.

• In August 2022, Nexus Spine announced the full commercial launch of its PressON posterior lumbar fixation system. PressON rods are designed to press onto pedicle screws rather than set screws. This unique biomechanically stronger design measures approximately one-quarter the size of standard systems. The rods are implanted faster, and they avoid the chance of set screw loosening and allow for intraoperative rod assembly for patients. The complete market release allowed the company to expand its compliant mechanism-based portfolio, which includes a range of flexible Tranquil titanium interbody fusion devices that are offered after an exhaustive validation period of refinements and system improvements.

• In October 2021, NuVasive Inc launched the Cohere TLIF-O implant. With the addition of the Cohere TLIF-O implant to its Advanced Materials Science (AMS) portfolio, NuVasive has become the only company to provide both porous PEEK and porous titanium implants for posterior spinal surgery.