Pluggable Optics for Data Center Market

Adoption of Linear Pluggable Optics to Fuel Pluggable Optics for Data Center Market Growth

Linear pluggable optics (LPO) are optical transceivers that do not include digital signal processor (DSP) chips. They rely on simpler signal modulation techniques and basic electronic components. This results in lower power consumption and production costs compared to DSP-based solutions. This simplicity also results in lower latency, making LPOs suitable for high-speed environments. LPO modules are increasingly being used in modern data centers, and they are becoming essential components of co-packaged optics (CPO) and near-package optics (NPO) solutions. These applications benefit from direct, short connections between ICs and LPO optical modules, which maximize the efficiency gains provided by LPO technology:

Lower power consumption, reduced bill of material (BOM) components, and minimal latency features of LPOs are expected to fuel their demand in the coming years. In addition, mega data centers widely adopt LPO, and it works great for latency-sensitive applications in AI and ML and enhances network performance. To cater to this market, the market players are launching solutions, which contribute to the market growth. For example, in March 2023, Eoptolink Technology Inc., Ltd. (SZSE: 300502)—a leading provider of optical transceiver solutions and services—announced the launch of 800G LPO. The product was launched due to the measurable cost savings offered by LPO to the mega data center.

LPO significantly reduces power consumption for both the module and the system while maintaining a pluggable interface, providing the economics and flexibility customers require for high-volume deployments. The industry leaders are focused on the reduction of the network power consumption for AI and other high-performance applications. For that, they are taking some strategic decision that maximizes the adoption of LPO technology. In March 2024, the Linear Pluggable Optics Multi-Source Agreement (LPO MSA) was formed by a group of networking, semiconductor, and optics companies to develop specifications for networking equipment and optical modules that will enable a broad ecosystem of interoperable LPO solutions. Accelink, Arista, AMD, Broadcom, Eoptolink, Hisense, Cisco, Innolight, MACOM, Intel, NVIDIA, and Semtech are the founding members of the LPO MSA. Such consortium to define LPO specifications drives the pluggable optics for data center market

Pluggable Optics for Data Center Market: Industry Overview

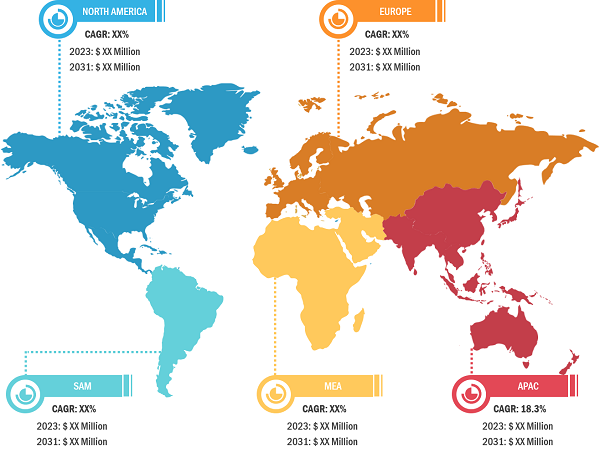

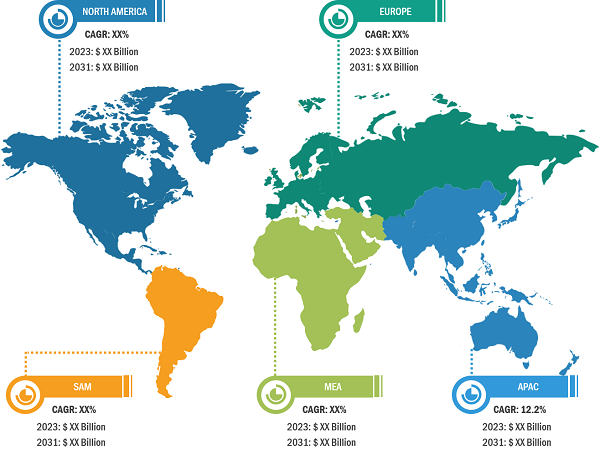

The pluggable optics for data center market analysis has been carried out by considering the following segments: components and data rate. In terms of component, the market is segmented into switches, routers, and servers. Based on data rate, the market is categorized into 100–400 Gb/s, 400–800 Gb/s, and 800 Gb/s and above. Geographically, the pluggable optics for data center market is segmented into North America, Europe, Asia Pacific (APAC), the Middle East & Africa (MEA), and South America (SAM).

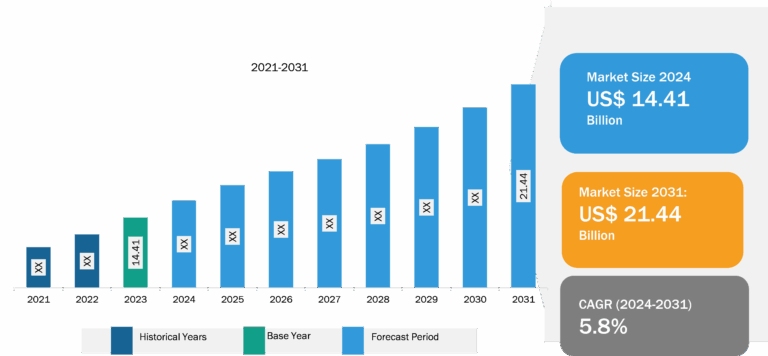

UK held a significant Pluggable Optics for Data Center market share in 2023.

The UK pluggable optics for data center market is growing rapidly with the increasing investment in data centers and the presence of key IT companies, including Google LLC, Microsoft Corp, Oracle Corp, SAP SE, and IBM Corp. These players are making significant investments to develop and advance their data centers. For instance, in January 2024, Google LLC announced an investment of US$ 1 billion in a new UK data center in Waltham Cross, Hertfordshire. This investment will provide critical computing capacity to businesses across the UK, fostering AI innovation and ensuring dependable digital services for Google Cloud customers and users in the UK and worldwide. Increasing focus on data center capacity expansion surges the adoption of pluggable optics for faster data processing and real-time analytics.

Pluggable Optics for Data Center Market Analysis: Competitive Landscape and Key Developments

The pluggable optics for data center market report emphasizes the key factors driving the market and prominent players’ developments. Coherent Corp, Nokia Corp, Cisco Systems Inc, Infinera Corp, Telefonaktiebolaget LM Ericsson, Ciena Corp, Intel Corp, Lumentum Holdings Inc, Juniper Networks Inc, Marvell Technology Inc, Yangtze Optical Fibre and Cable Joint Stock Ltd, and Broadcom Inc are among the prominent players profiled in the pluggable optics for data center market report. The market players focus on new product launches, expansion and diversification, and acquisition strategies, which allow them to access prevailing business opportunities. A few of the key market developments are listed below:

- In March 2024, Nokia Corp announced a comprehensive set of new optical transport solutions optimized for metro edge deployments for CSP, webscale and Enterprise customers. The company’s portfolio additions include 100Gb/s, 400Gb/s and 800Gb/s pluggable coherent modules, a new compact optical transport platform and new cards optimized for metro edge applications.

- In April 2024, Infinera announced that Aire Networks, a subsidiary of Grupo Aire, deployed Infinera’s software-programmable ICE-X coherent pluggable solution to expand the capacity of its single-fiber network infrastructure across Spain and Portugal. The ability of Infinera’s innovative ICE-X solution to provide ultra-high-speed transmissions over a single fiber in a pluggable form factor enables Aire Networks to continue to meet the bandwidth demands of its customers while maintaining its cost-effective single-fiber infrastructure.

- In September 2023, Infinera and Sumitomo Electric Industries, Ltd. announced the successful completion of the first demonstration delivering high-speed business services over Sumitomo Electric’s passive optical network (PON) infrastructure with Infinera’s ICE-X intelligent, coherent pluggable optics. The demonstration validated how Sumitomo Electric can leverage next-generation coherent pluggables to provide improvements to network efficiencies and expand capacity while also enabling new high-speed business services and supporting next-generation applications such as 5G and edge computing.