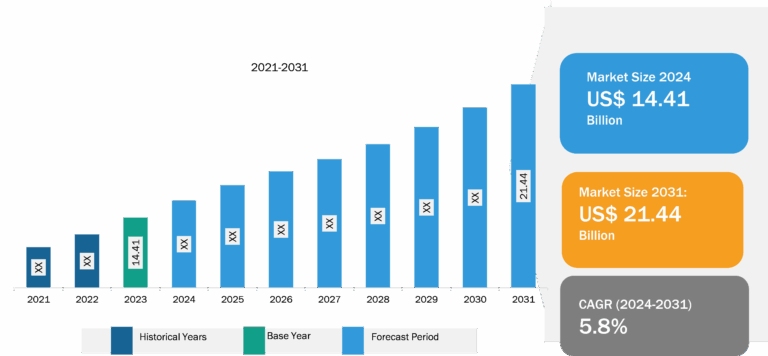

Power Electronics Market

Conventional power electronics rely on silicon semiconductor technologies that typically have an efficiency of 85–95%, which causes a loss of approximately 10% of the electrical energy in the form of heat. The electrical field strength of silicon carbide (SIC) devices is approximately ten times stronger (2.8MV/cm vs. 0.3MV/cm) than silicon semiconductors. The SiC substrate can have a thinner layer structure, thermal design, and high-power densities, with high frequency switching that helps in reducing power dissipation in electric cars. The SiC-based power electronics devices have three times greater thermal conductivity and can function at higher temperatures, which increases its demand in electric vehicles for controlling heat. The demand for electric vehicles is growing across the globe. For instance, according to the International Energy Agency (IEA), electric vehicle sales increased by 10 million in 2022; approximately 14% of all new cars sold across the globe were electric, as compared to 2020. The increasing sales of electric cars globally is a key factor boosting the adoption of power electronics among automotive manufacturers. These devices are used to control heat and manage electricity in the charging and discharging of electric vehicles. SiC-based power electronics provide users with reliable and efficient energy management, which fuels the global power electronics market growth.

UK Dominates Power Electronics Market in Europe

The power electronics industry in the UK is experiencing massive growth, driven by factors such as a surge in growth for renewable energy, the development of electric vehicles, and an increased need for more efficient industrial processes. The UK government has identified power electronics as a key technology for future economic growth. It has implemented several initiatives to support the industry, including the Advanced Propulsion Centre (APC) and the Driving the Electric Revolution Industrialization Centre (DERIC). Additionally, the UK government has set a target for all new cars and vans to be zero-emission by 2035. For instance, in September 2023, the zero-emission vehicle (ZEV) mandate was unveiled. The country will have the most widespread regulatory framework for the switch to EVs globally. The framework requires 80% of new cars and 70% of new vans to be sold in Great Britain in order to achieve zero emissions by 2030, which is expected to reach 100% by 2035. All these factors are driving the need for power electronics technologies that can be utilized in electric vehicles, such as inverters, converters, and battery management systems.

The power electronics market growth in the automotive industry in Germany is experiencing significant growth. Germany is a leading market for EVs and HEVs, with the government setting ambitious goals for their adoption. For instance, in 2022, over 350,000 fully electric cars were registered in Germany, recording the highest figure, according to ACEA data. This has led to increased demand for power electronics components, such as inverters, converters, and battery management systems.

Segmental Overview

Based on type, the power electronics market is classified into power discrete, power module, and power IC. The power module segment recorded the largest power electronics market share in 2022, whereas the power IC segment is anticipated to record the highest CAGR during the forecast period. Based on material, the power electronics market is segmented into silicon (SI), silicon carbide (SIC), gallium nitride (GAN), and others. The silicon (SI) segment recorded the largest power electronics market share in 2022 while the silicon carbide (SIC) segment is anticipated to record the highest CAGR during the forecast period. Based on industry vertical, the power electronics market is segmented into ICT, automotive & transportation, consumer electronics, industrial, energy & power, and others. The consumer electronics segment held the largest power electronics market share in 2022, while the ICT segment is likely to record the highest CAGR during the forecast period.

Market Analysis: Competitive Landscape and Key Developments

- In November 2023, Mitsubishi Electric Corporation announced that it will enter into a strategic partnership with Nexperia B.V. to develop silicon carbide (SiC) power semiconductors for the power electronics market. Mitsubishi Electric will leverage its wide-bandgap semiconductor technologies to develop and supply SiC MOSFET chips that Nexperia will use to develop SiC discrete devices.

- In October 2023, Infineon Technologies AG opened a new laboratory for the development of quantum electronics in Oberhaching near Munich. The objective is to develop and test microelectronic circuits for quantum computers that will be stable and small, will operate reliably, and can be produced on an industrial scale. Approximately twenty researchers will work at the lab. In addition to quantum computing, activities will also focus on the development of AI algorithms for the early detection of variances in power systems.

- In October 2023, Littelfuse, Inc., an industrial technology manufacturing company empowering a sustainable, connected, and safer world, announced the release of IXTY2P50PA—the first automotive-grade Polar P-Channel Power MOSFET. This innovative product design meets the demanding requirements of automotive applications, providing exceptional performance and reliability.