Trauma and Extremities Devices Market

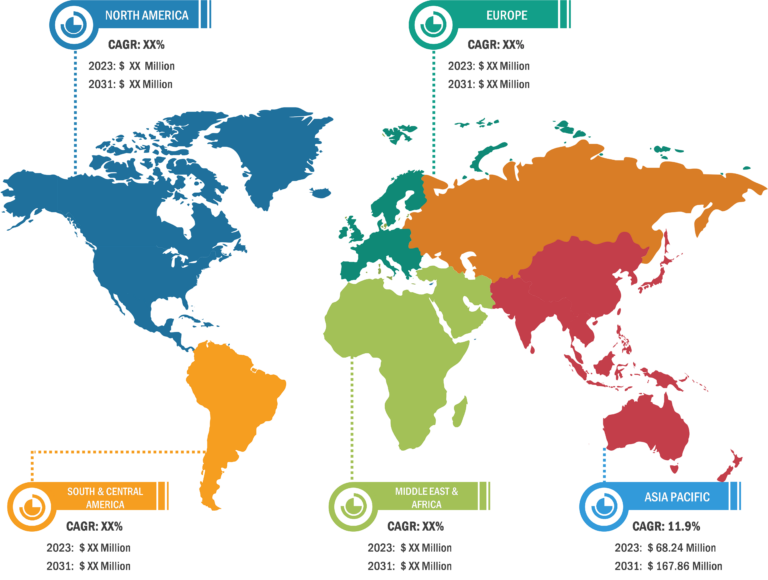

Asia Pacific is the fastest-growing region in the trauma and extremities devices market primarily due to growing incidences of osteoporosis—a medical condition that weakens the bones, making them brittle and more likely to break. It is characterized by the deterioration of bone microarchitecture and reduced bone density. According to the Asian Federation of Osteoporosis Societies study in 2018, the burden of fragility fractures is especially high in Asia Pacific, and projections indicate a significant increase in hip fractures from 1,124,060 cases in 2018 to 2,563,488 cases by 2050. Therefore, trauma and extremities devices become crucial to address realignment and fixation for proper healing in case of severe fractures. Further, sports injuries, road accidents, and geriatric population support the growth of the trauma and extremities devices market in the region.

Growing Cases of Osteoporosis in Adults and Neonates Drive Trauma and Extremities Devices Market Growth

Osteoporosis is an increasingly common health issue affecting adults and newborns, a disorder marked by weakened and fragile bones. According to the International Osteoporosis Foundation 2022, osteoporosis causes more than 8.9 million fractures every year globally, resulting in osteoporotic fractures every 3 seconds. Newborns also develop osteoporosis, especially preterm babies. They are more prone to fractures since their bones are immature and weak. According to the Journal of Neurodevelopmental Disorders, over the last few decades, there has been an increase in the recognition of osteoporosis in children. Both genetic and acquired bone disorders in children can weaken their bones. If these conditions are not treated, they can cause reduced bone mass and deformities, thereby impacting the quality of life. Thus, the growing cases of osteoporosis in adults and children propel the demand for trauma and extremities devices. 56349

Trauma and Extremities Devices Market: Segmental Overview

Based on device type, the market is segmented into internal fixation devices, external fixation devices, craniofacial devices, long bone stimulation, and other trauma devices. The internal fixation devices segment held the largest market share in 2023.

Based on end user, the trauma and extremities devices market is segmented into hospitals, clinics, and others. The hospitals segment is anticipated to hold a significant market share during 2023–2031. These organizations employ teams of skilled staff to provide care with the use of sophisticated medical devices and equipment. Therefore, hospitals are the primary end users of trauma and extremities devices.

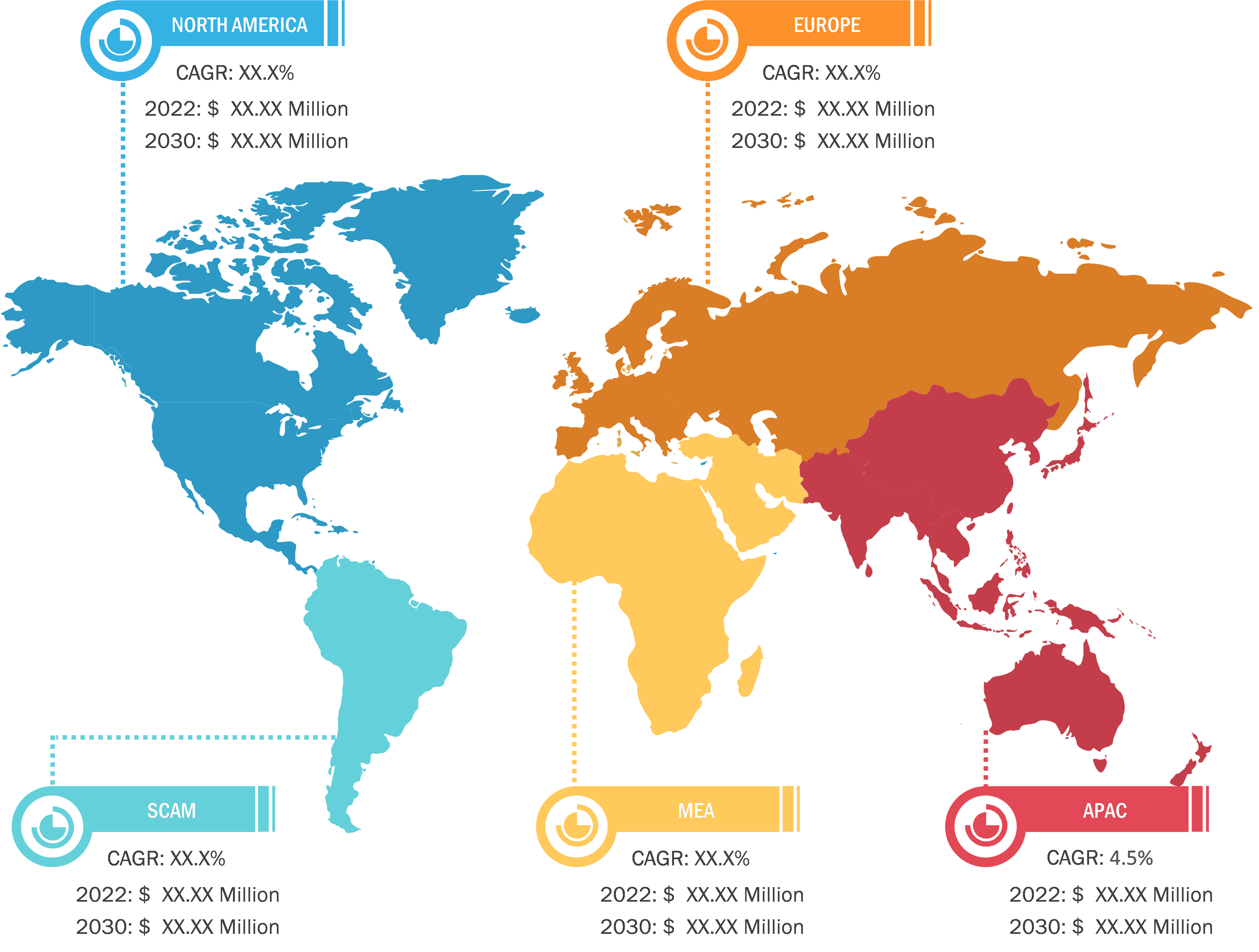

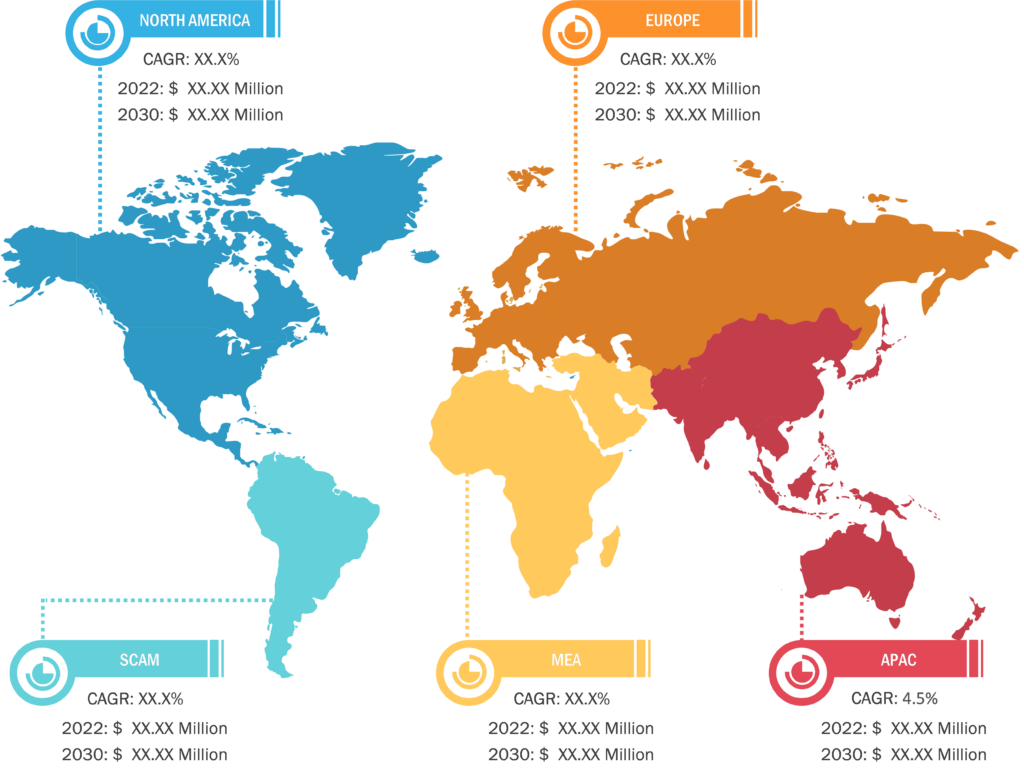

Geographically, the trauma and extremities devices market report is segmented into North America (the US, Canada, and Mexico), Europe (Germany, France, Italy, the UK, Russia, and the Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and the Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

Aortic Stent Grafts Market: Competitive Landscape and Key Developments

Stryker, Zimmer Biomet, Smith & Nephew, Wright Medical Group N.V, Advanced Orthopaedic Solutions, Integra LifeSciences Corporation, Acumed LLC, Orthofix Holdings, Inc, Medartis AG, Corin, Matrix Meditec Private Limited, Electramed Ltd., and Miraclus are a few key companies operating in the trauma and extremities devices market. These companies adopt product innovation strategies to fulfill evolving customer demands, which allows them to maintain their brand name in the trauma and extremities devices market.

As per press releases by key players operating in the market, a few initiatives are listed below:

- In March 2023, Stryker launched its Gamma4 Hip Fracture Nailing System in most European markets. This newest Gamma system is designed to provide surgeons with the next generation of Stryker’s intramedullary nailing system, and it is specifically designed to treat hip and femur fractures. The Gamma4 system aims to streamline procedural workflows for surgeons. In September 2023, the system received CE certification in Europe.

- In September 2023, Orthofix Medical Inc. announced the US commercial launch of the Galaxy Fixation Gemini system. This latest addition to the Galaxy product line is a stable external fixation system available in several sterile procedure kit configurations. It provides a quick solution for treating fractures caused by trauma in the upper and lower limbs.

- In December 2021, the Johnson & Johnson Medical Devices Companies announced that DePuy Synthes, through its affiliate Synthes GmbH, acquired OrthoSpin, Ltd., an Israeli company. OrthoSpin is known for developing and manufacturing an automated strut system, which is used alongside DePuy Synthes’ MAXFRAME Multi-Axial Correction System, an external ring fixation system.

- In November 2021, DePuy Synthes, The Orthopaedics Company of Johnson & Johnson, launched the UNIUM™ System as the newest addition to its Power Tools portfolio. The system is designed with a commitment to ergonomics, reliability, and efficiency in the Trauma setting. It can be used across small bones, sports medicine, spine, and thorax procedures.

- In October 2021, Smith+Nephew completed the acquisition of Integra LifeSciences Holdings Corporation’s Extremity Orthopaedics business for US$ 240 million. This acquisition substantially enhanced Smith+Nephew’s extremities business by providing a dedicated sales channel, complementary shoulder replacement, and upper and lower extremities product portfolio, as well as an exciting new product pipeline.