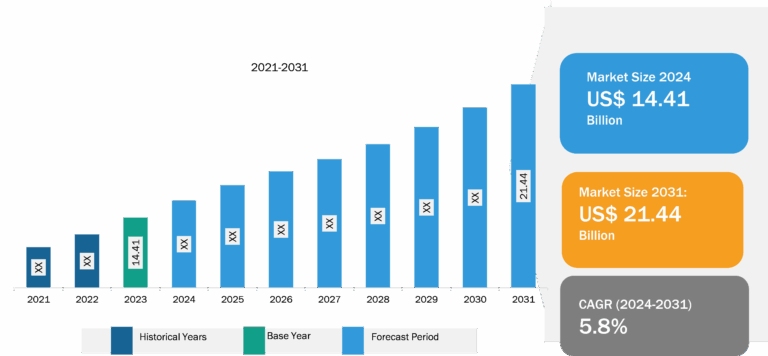

Occlusion Devices Market

The occlusion devices market in Asia Pacific is expected to grow at the highest CAGR during the forecast period. North America accounted for the largest share of the market in 2023. The surging prevalence and incidence of cardiovascular diseases is a major factor fueling the growth of the market. The growing preference for minimally invasive surgeries, availability of better healthcare infrastructure, and the rising number of new occlusion device approvals are the factors bolstering the overall growth of the market. In November 2020, Abbott Laboratories received FDA approval for its Amplatzer Piccolo Occluder, which is the world’s first medical device that can be implanted in babies using a minimally invasive procedure to treat patent ductus arteriosus. Therefore, contributions and market initiatives of the key players such as Abbott, Johnson & Johnson, and MicroPort Scientific Corporation are positively influencing the occlusion devices market growth in North America.

Cardiovascular diseases, including coronary artery disease, arrhythmia, and chronic total occlusion (CTO) can restrict the blood flow to the heart, causing a cardiac arrest or stroke. Based on angiographic evidence, a CTO is a complete coronary artery blockage that persists for 3 or more. According to the Centers for Disease Control and Prevention (CDC), in 2021, coronary heart disease was the most prevalent type of heart disease, affecting ~5% of adults aged 20 and above, and it resulted in the death of 375,476 people in the US. Occlusion devices are specialized tools or implants used to block abnormal blood vessels or structural defects in the heart. The occlusion device is designed with an expandable tubular body that consists of a frame with multiple interconnected parts. This frame expands inside a blood vessel and collapses for the delivery or retrieval of the device. In addition, the device features a hydrophilic polyurethane hydrogel layer attached to the interconnected components of the tubular expandable body. The polyurethane hydrogel layer expands when the device comes in contact with an aqueous environment.

Occlusion devices such as occlusion balloons, stent retrievers, and embolization devices are commonly used in interventional procedures, including angioplasty and thrombectomy, to remove blockages in blood vessels. The rising incidences of CTOs have led to an increase in the number of CTO percutaneous coronary interventions (PCIs) for the management of occlusion of arteries. Thus, the prevalence of acute and chronic heart diseases propels the occlusion devices market growth.

The rising number of product recalls in the occlusion devices market has raised concerns among healthcare providers and patients. These recalls can be a result of factors such as design flaws, manufacturing defects, or inadequate safety standards. As consequence to recalls, trust in certain brands and products may diminish, leading to a potential decline in demand for aortic valve replacement devices. Patients and medical professionals may become more cautious while considering these devices, preferably opting for alternatives or delaying procedures.

A few product recalls by key players in the occlusion devices market are mentioned below:

• In June 2023, Baxter Healthcare Corporation issued a recall for the SIGMA Spectrum Infusion Pumps with Master Drug Library and Spectrum IQ Infusion Systems with Dose IQ Safety Software. The recall was due to repeat upstream occlusion false alarms, which can interrupt or delay therapy and contribute to clinician fatigue, which may cause serious adverse health consequences, especially for people receiving life-sustaining medications.

• In July 2021, W. L. Gore & Associates, Inc. initiated a voluntary product recall of GORE Molding and Occlusion Balloon Catheters intended for the temporary occlusion of aortic vessels or for assisting the expansion of endovascular prostheses. The company identified a change in manufacturing equipment as the source of the device failure.

Occlusion Devices Market: Segmental Overview

By product, the market is segmented into occlusion removal devices, embolization devices, and support devices. The occlusion removal devices segment is further categorized into stent retrievers, coil retrievers, balloon occlusion devices, and suction and aspiration devices. The embolization devices segment is subsegmented into embolic coils, liquid embolic agents, and tubal occlusion devices. The support devices segment is further bifurcated into microcatheters and guidewires. The occlusion removal devices segment held the largest occlusion devices market share in 2023. This is attributed to an increasing number of patients with chronic total occlusion, which creates a demand for diagnoses and treatments. Further, the support devices segment is anticipated to register the highest CAGR during the forecast period.

The market, by application, is categorized into neurology, cardiology, peripheral vascular diseases, urology, oncology, and gynecology. The cardiology segment held the largest share of the occlusion devices market in 2023. The implantation of occlusion devices has become a widely accepted and highly effective treatment for occluding abnormal blood/thrombus flow within the heart. The cardiology segment is further anticipated to register the highest CAGR during the forecast period.

The market, by end user, is categorized into hospitals, diagnostic centers and surgical centers, ambulatory care centers, and research laboratories and academic institutes. The hospitals segment held the largest share of the occlusion devices market in 2023, and it is anticipated to register the highest CAGR during the forecast period. The rising adoption of minimally invasive surgical procedures, and the availability of reimbursements for targeted procedures and diagnoses in developed countries are the key factors driving the growth of the market for this segment.

The occlusion devices market report, based on geography, is segmented into North America (US, Canada, and Mexico), Europe (Germany, France, Italy, UK, Russia, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), the Middle East & Africa (South Africa, Saudi Arabia, UAE, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Occlusion Devices Market: Competitive Landscape and Key Developments

Abbott; Boston Scientific Corporation; LeMaitre Vascular, Inc; Edwards Lifesciences Corporation; Medtronic; MicroPort Scientific Corporation; Johnson & Johnson; Terumo Group; Stryker Corporation; and Tokai Medical Products are among the prominent players profiled in the occlusion devices market report. These companies adopt product innovation strategies to meet evolving customer demands, which allows them to maintain their brand name in the market.

A few of the strategic developments by leading players operating in the occlusion devices market, as per company press releases, are listed below:

• In February 2024, BIOTRONIK and Interventional Medical Device Solutions (IMDS) partnered to launch an innovative Micro Rx catheter. It is a rapid exchange microcatheter designed to enhance guidewire support during percutaneous coronary interventions (PCI). This advanced device is exclusively distributed by BIOTRONIK and manufactured by IMDS.

• In September 2023, MicroPort Endovastec announced the successful implantation of the Reewarm PTX Drug Coated Balloon (DCB) Catheter by a team of doctors at Paulo Sacramento Hospital in Sao Paulo, Brazil. This shows the product’s continued proliferation in international markets. This device is intended to treat stenosis or occlusion in the femoral-popliteal artery for percutaneous transluminal angioplasty (PTA) in the peripheral vessels.