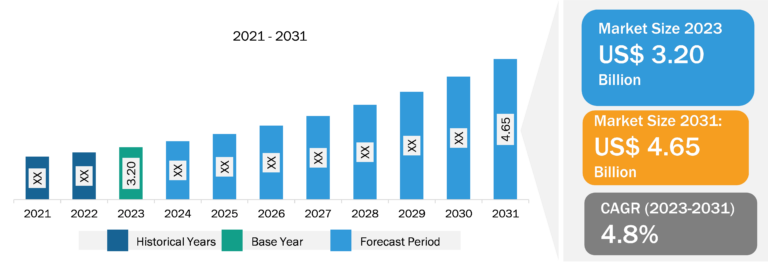

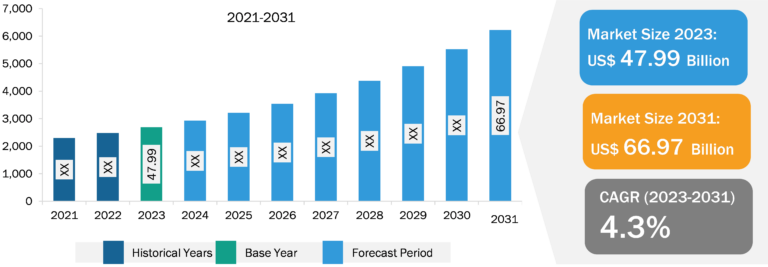

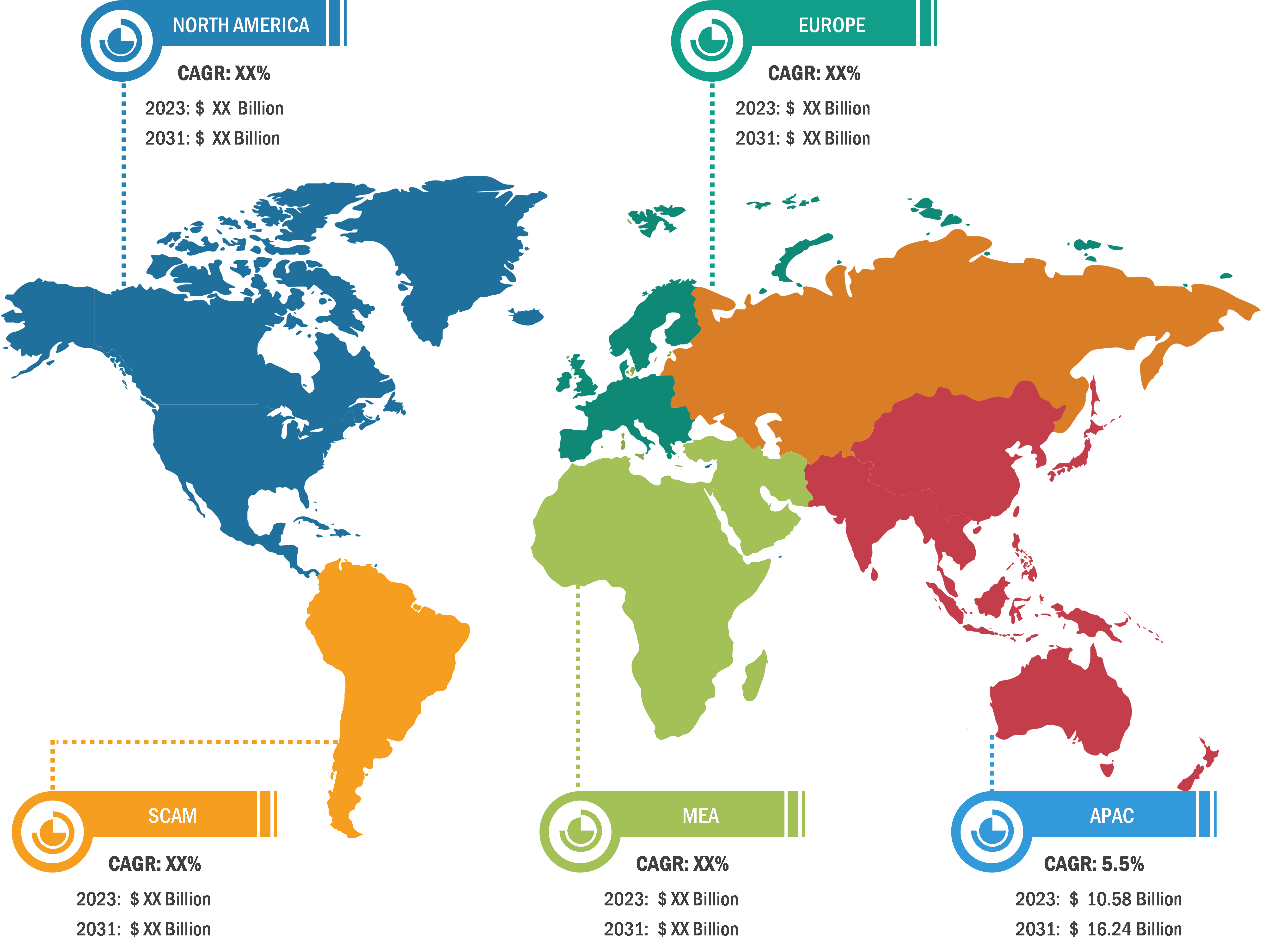

Pulmonary Drug Delivery Systems Market

Pulmonary drug delivery refers to the systems that target the delivery of aerosols directly to epithelial cells and respiratory epithelium through inhalation. These systems deliver the drug to the lungs to treat respiratory diseases. It is one of the most preferred drug delivery routes and a noninvasive technique with a large surface area of absorption and blood circulation. Also, high permeability rate makes this technique an ideal method for treating respiratory diseases. It provides direct access to the site of disease for treating respiratory diseases without the inefficiencies and unwanted effects of systemic drug delivery. The increasing burden of respiratory diseases and growing strategic initiatives by companies contribute to the growing pulmonary drug delivery systems market size. However, regulatory issues associated with the approval of pulmonary drug delivery systems hinder market growth. Moreover, the advancements in inhaler technologies are expected to bring new pulmonary drug delivery systems market trends in the coming years.

Increasing Burden of Respiratory Diseases Drives Pulmonary Drug Delivery Systems Market Growth

Chronic obstructive pulmonary disease (COPD), asthma, cystic fibrosis, and other respiratory diseases can lead to severe illness, acute respiratory failure, or death. Urbanization, pollution, unhealthy lifestyles, and high tobacco consumption are among the leading factors contributing to the growing cases of respiratory disease. COPD is anticipated to become the leading cause of death across the world in the next 15 years. According to the National Center for Biotechnology Information, it is a disease spectrum that includes bronchitis and emphysema and is becoming a significant health and economic crisis.

As per a report published by the Global Initiative on Chronic Obstructive Lung Disease, ~65 million people suffer from COPD, and about 3 million people die from the disease yearly worldwide, making it the third leading cause of mortality globally. As per the 2023 American Lung Association data, ~34 million Americans are affected by chronic lung diseases such as asthma and COPD. As per the Office of Disease Prevention and Health Promotion, in the US, ~14.8 million adults were diagnosed with COPD in 2020. Similarly, in 2022, 4.6% of the adult population in the US was diagnosed with COPD, emphysema, or chronic bronchitis. As per Statistics Canada, 2 million people have COPD, which can impair a person’s capacity to breathe. As per the World Health Organization (WHO) estimates, COPD will become one of the major leading causes of death across the world by 2030. Growing cases of COPD fuel the growth of the pulmonary drug delivery systems market.

Furthermore, according to the WHO 2023 data, asthma affected ~262 million people and caused 455,000 asthma-related deaths in 2019. The British Lung Foundation reports that ~8 million people have a diagnosis of asthma in the UK. In addition, the Asthma and Allergy Foundation of America 2023 states that ~26 million people in the US had asthma in 2022, i.e., about 1 in 13 people in the country. Per the same source, ~3,517 death cases were recorded due to asthma in 2021. Additionally, the Asthma and Allergy Foundation of America also reported that asthma resulted in about 1.5 million emergency department visits and 4.9 million doctors’ office visits in 2019.

As per the March of Dimes Organization, there were between 70,000 and 165,000 cases of cystic fibrosis globally in 2019. According to the American Lung Association’s November 2022 estimates, ~30,000 people are affected by cystic fibrosis in the US. According to the Cystic Fibrosis Foundation, ~1,000 new cases of cystic fibrosis are diagnosed annually in the US. Pulmonary drug delivery offers targeted treatment for respiratory diseases such as asthma and COPD. Therefore, the increasing prevalence of respiratory diseases has increased the demand for pulmonary drug delivery systems, driving the pulmonary drug delivery systems market growth.

Pulmonary Drug Delivery Systems Market: Segmental Overview

The pulmonary drug delivery systems market is segmented on the basis of product, indication, distribution channel, and end user. Based on indication, the market is segmented into chronic obstructive pulmonary diseases, asthma, cystic fibrosis, and others. The chronic obstructive pulmonary diseases segment held a significant pulmonary drug delivery systems market share in 2023 and is projected to register the highest CAGR during 2023–2031. COPD is a recurring inflammatory lung disease that causes restricted airflow from the lungs and breathing problems. Its symptoms include mucus production, cough, breathing difficulty, and wheezing. It is usually triggered by long-term exposure to irritating gases or particulate matter, including cigarette smoke and air pollution. People affected by COPD are at a higher risk of developing lung cancer, heart disease, and various other conditions. According to the WHO, COPD is the third leading cause of death globally. In 2019, ~3.23 million deaths are reported globally due to COPD. According to the Office of Disease Prevention and Health Promotion, ~14.8 million US adults were diagnosed with COPD in 2020. Also, the National Health Service states that ~1.17 million people in the UK (i.e., ~1.9% of the total population) were detected with COPD in 2021. It is a considerable cause of morbidity and mortality in the UK, leading to 24 million lost working days, 30,000 deaths yearly, and an annual cost to the national health services of over US$ 966.87 million (£800 million).

Pulmonary Drug Delivery Systems Market: Competitive Landscape and Key Developments

AstraZeneca, GlaxoSmithKline Plc, Novartis AG, Koninklijke Philips NV, Boehringer Ingelheim International GmbH, Cipla Inc., OMRON Corp., PARI GmbH, Glenmark Pharmaceuticals, and Gilbert Technologies are a few key companies operating in the market. These companies focus on product innovation strategies to meet evolving customer demands, along with maintaining their brand name in the pulmonary drug delivery systems market.

A few recent developments initiated in the global pulmonary drug delivery systems market report are mentioned below:

- In January 2023, Avillion LLP announced that the US Food and Drug Administration (FDA) approved AstraZeneca’s Airsupra (formerly known as PT027) for the treatment of bronchoconstriction and to prevent or reduce the risk of exacerbations in people having asthma aged 18 years and above. In 2018, AstraZeneca and Avillion entered into a co-development partnership for PT027. Airsupra is a first-in-class, pressurized metered-dose inhaler, fixed-dose combination rescue medication containing albuterol and budesonide, an anti-inflammatory inhaled corticosteroid.

- In June 2021, Glenmark Pharmaceuticals Ltd became one of the first companies to introduce Tiogiva, a bioequivalent version of Tiotropium Bromide dry powder inhaler for the treatment of COPD in the UK. It is the second inhalation product in-licensed by the company for the European market after the Stalpex (Fluticasone/ Salmeterol) dry powder inhaler.

- In September 2020, the FDA approved GSK’s Trelegy Ellipta to treat asthma and COPD in the US. Trelegy is the only single inhaler triple therapy available for patients in a convenient once-daily inhalation in the country.