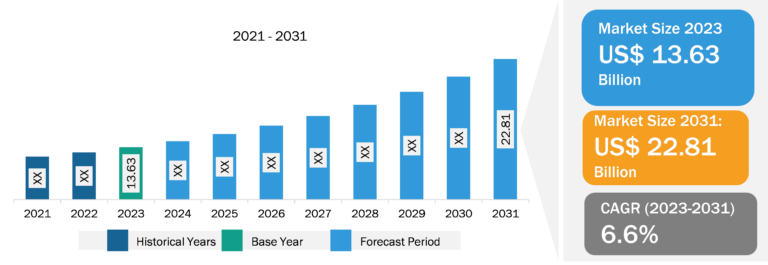

Safety Instrumented System Market

According to the Cefic, the European Chemical Industry Council, the region is the second-largest producer of chemicals in the world. The sales of chemicals in the European Union (EU) stood at US$ 631.82 billion (EUR 594 billion), while in the Rest of Europe, it was ~US$ 177.63 billion (EUR 167 billion) in 2021. According to the same report, the EU contributed 15% of the global shares in 2021 in world chemical sales. Of the total chemical sales of the EU, petrochemicals accounted for 26%, and the remaining 74% was from basic inorganic (13%), polymers (20%), specialty chemicals (27%), and consumer chemicals (14%). Also, around two-third of the chemical sales came from the four member states—Germany (29%), France (17%), Italy (10%), and the Netherlands (10%). This growing chemical production and sales is rising need for a high-end safety system to protect the plant assets and employees from any dangerous situation.

It has been observed that the pharmaceutical industry is a major contributor to the EU economy. The European Federation of Pharmaceutical Industries and Associations (EFPIA), in its 2022 report, estimated that the pharma production in the region was valued around US$ 320.25 billion (EUR 300 billion), which rose from US$ 306.04 billion (EUR 286.69 billion) in 2020. In addition, pharma companies are constructing new manufacturing plants to promote the growth of the European pharmaceutical sector. In May 2022, Bayer AG announced to initiate the construction of a new pharmaceutical facility in Leverkusen, Germany. The facility will manufacture medicinal products for the treatment of cardiovascular diseases and cancer. This new US$ 286.14 million (EUR 275 million) worth facility will be operational in 2024. Similarly, in March 2023, BluePharma announced that they had opened an oral solid high-potency drug manufacturing facility in Portugal. It is one of the largest drug manufacturing facilities in Europe, for which an investment of US$ 31.69 million (EUR 30 million) was made. Thus, the growing construction of new pharma production facilities in the region is expected to raise the need for safety instrumented systems as it can help bring dangerous processes to a safe state in pre-determined hazard scenarios and keep people within and near the operational site safe. Thus, all the factors mentioned above drive the safety instrumented system market growth in Europe.

India Recorded Largest CAGR in Safety Instrumented System Market

India is one of the largest manufacturers of pharmaceuticals. According to Invest India, the Indian pharma industry ranks third in pharmaceutical production by volume in the world. Also, the sector contributed around 1.32% of the gross value added (GVA) to the Indian Economy during 2020–2021. Also, India is one of the world’s biggest suppliers of low-cost vaccines. It accounts for 60% of global vaccine production, contributing upto 70% of the WHO demand for Tetanus, Diphtheria, Pertussis (DPT), and Bacillus Calmette–Guérin (BCG) vaccines and 90% of the WHO demand for the measles vaccine. In addition, the country is the largest provider of generic medicines across the world, occupying a 20% share of global supply by volume. It manufactures almost 60,000 different generic brands across 60 therapeutic categories. Moreover, the country has the highest number of US-FDA-compliant pharma plants outside the US and is home to more than 3,000 pharma companies with around 10,500 manufacturing facilities. Furthermore, according to Invest India, the Indian pharmaceutical industry is expected to reach US$ 65 billion by 2024 and US$ 130 billion by 2030. Thus, the growing pharmaceutical industry in India is expected to fuel the safety instrumented system market growth in the country during the forecast period.

Safety Instrumented System Market Segmental Overview

Based on application, the safety instrumented system market is divided into emergency shutdown systems, fire and gas monitoring and control, high integrity pressure protection systems, burner management systems, and turbo machinery control. The emergency shutdown systems segment held the largest safety instrumented system market share in 2022 and is anticipated to register the highest CAGR during 2022–2030. In terms of end user, the safety instrumented system market is categorized into chemicals & petrochemicals, oil & gas, power generation, pharmaceutical, food & beverages, and others. The chemicals & petrochemicals segment held the largest safety instrumented system market share in 2022 and the oil & gas segment is anticipated to register the highest CAGR during 2022–2030.

Safety Instrumented System Market Analysis: Competitive Landscape and Key Developments

ABB Ltd, Applied Control Engineering Inc, AVEVA Group plc, Emerson Electric Co, HIMA, Honeywell International, Rockwell Automation Inc, Schneider Electric, Siemens AG, and Yokogawa Electric Corporation are among the key safety instrumented system market players profiled in the report. Several other essential safety instrumented system market players were also analyzed for a holistic view of the market and its ecosystem. The market report provides detailed market insights to help major players strategize their growth.

- In October 2021, Emerson introduced the first valve assemblies that meet the design process requirements of Safety Integrity Level (SIL) 3 per the International Electrotechnical Commission’s IEC 61508 standard. These Fisher Digital Isolation final element solutions serve the needs of customers for shutdown valves in critical safety instrumented system (SIS) applications.

- In February 2021, ECI announced that they have partnered with Profire Energy to deliver burner management controls and solutions. Under this partnership, ECI provides burner management solutions that maintain optimal burner functionality and temperature control for process heaters. These burner management systems enable safe and reliable operations, minimize downtime, and aid in maintaining regulatory compliance.