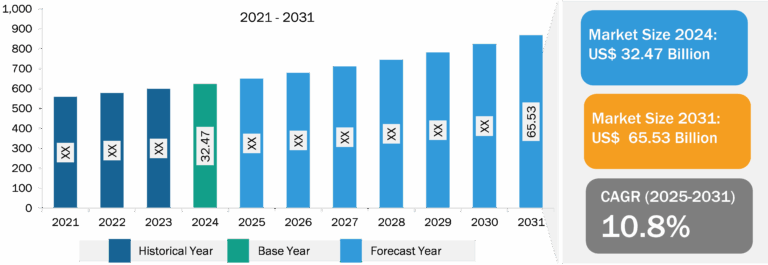

Mortar Systems Market

The changing modern warfare scenario has obligated governments of various countries to allocate significant funds and financial aid to respective defense and military forces. The defense budget allocation supports army and military forces in purchasing technologies and equipment from domestic or international developers. There is an augmented need to reinforce defense and military forces with advanced ground warfare systems; hence, land forces across the globe are focusing on investing significant amounts in procuring ground artillery systems such as mortars, rocket artillery, and howitzers. Defense forces’ constant inclination to acquire new technologies for non-combat and combat operations further boosts military expenditure worldwide which is also acting as one of the major mortar systems market trends across different regions.

The conflict between Russia and Ukraine prompted a shift in defense priorities for a few European nations. As part of the NATO alliance, European countries have shown solidarity with Ukraine and increased their support to reinforce NATO’s eastern flank. This involved boosting defense spending to meet NATO commitments and enhance collective defense capabilities. The conflict prompted greater collaboration among European nations in defense cooperation and joint capability development.

European Union member states recognize the benefits of collaborative procurement to achieve cost reductions, economies of scale, and interoperability. Joint procurement framework contracts, such as those approved by the European Defence Agency (EDA), underscore the commitment to shared defense objectives.

In September 2023, the European Defence Agency (EDA) approved eight joint procurement framework contracts for 155 mm ammunition, signifying a collaborative effort among European Union member states to replenish stocks and increase the supply of critical shells to Ukraine. This joint procurement approach, endorsed by 26 Member States and Norway, aims to achieve cost reduction through economies of scale and enhance interoperability. The flexible and inclusive EDA project allows all member states to participate in the initiative, ensuring the purchase of ammunition aligns with national needs or supports Ukraine.

In March 2023, Elbit Systems Ltd., a global defense technology company, announced two significant contracts. The first contract, valued at US$ 120 million, was awarded to its Romanian subsidiary, Elmet International SRL, by General Dynamics European Land Systems. The contract involves the supply of unmanned turrets, remote-controlled weapon stations (RCWS), and mortar systems for the “Piranha V” armored personnel carrier (APC) for the Romanian Armed Forces, with the work scheduled over a three-year period. The second contract, valued at ~US$ 21.61 million, was part of a defense export agreement between Israel and Montenegro Ministries of Defense. It includes the procurement of Elbit Systems-made weapons, specifically mortar systems and training equipment.

As per the Stockholm International Peace Research Institute (SIPRI), global military expenditure increased to US$ 2,148 billion in 2022, representing a 3.5% increase from 2021. The US, China, India, Russia, and Saudi Arabia were the top five spenders in 2022, accounting for 63% of global expenditures. The figure given below depicts the yearly spending of these countries.

Military Expenditure of Top Five Countries (2020–2022)

| Country | 2020 (US$ Million) | 2021 (US$ Million) | 2022 (US$ Million) |

| US | 778,397.2 | 800,672.2 | 876,943.2 |

| China | 257,973.4 | 293,351.9 | 291,958.4 |

| Russia | 61,712.5 | 65,907.7 | 86,373.1 |

| India | 72,937.1 | 76,598.0 | 81,363.2 |

| Saudi Arabia | 64,558.4 | 55,564.3 | 75,013.3 |

Source: SIPRI

The increasing military expenditure encourages incorporating advanced warfare technologies such as high-range antennas, self-propelled artillery including mortars, advanced communication devices, unmanned vehicles, radars, missile detection systems, surveillance and navigation systems, and modern warfare technologies. In addition, a high military budget supports the countries in assigning resources for the advancement and upgrade of their existing air, ground-based, and naval defense systems. Such factors have been boosting the mortar systems market growth across different regions.

Rising Contracts for the Procurement of Mortars and Mortar Munitions to Provide Lucrative Opportunities for Mortar Systems Market Size

One of the major factors driving the growth for mortar systems market includes the rising number of contracts for mortars including towed and self-propelled products. Below are some of the mortar systems and ammunitions procurement contracts that are driving the mortar systems market growth across different regions:

- In March 2023, Elbit Systems won a contract worth US$ 120 million for supplying the unmanned turrets, weapon stations and mortar systems to the Romanian Armed Forces.

- In November 2023, the German government awarded a contract to Rheinmetall AG for supplying 100,000 rounds of 120mm mortar ammunition to Ukraine.

- In 2January 2024, Milanion NTGS, the UK manufacturer of the Alakran deployable mortar system announced that its contract for supplying of Vehicle Mounted Infantry Mortar System (VMIMS) to the Indian army will get completed by the end of 2024.

- In September 2023, Elbit Systems UK won a contract from the UK Ministry of Defense for the development of artillery and mortar training simulators.

- In December 2019, the French defence procurement agency (DGA) awarded the sixth contract amendment on the SCORPION programme to the consortium formed by Nexter, Arquus and Thales. This latest award, known as MEPAC, covers the delivery of 54 additional Griffon multi-role armoured vehicles (VBMR) equipped with Thales’s 120-mm 2R2M (Rifled Recoiled Mounted Mortar) system, reaching the total number of Griffon vehicles on the SCORPION program to 1,872 in accordance with the Military Planning Law 2019-2025.

Such new procurement of mortars is providing new opportunities for mortar systems market players across different regions.

Mortar Systems Market: Segmental Overview

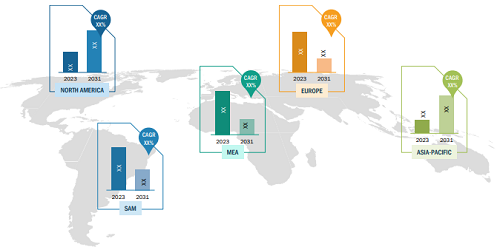

The mortar systems market is segmented based on calibre, type, and geography. In terms of calibre, the mortar systems market is categorized into small calibre, medium calibre, and large calibre. In 2022, medium calibre accounted for the largest mortar systems market share, and it is expected to retain its dominance during the forecast period as well. Based on type, the mortar systems market has been segmented into towed/hand held and self-propelled. In 2022, self-propelled segment accounted for a major share in the global mortar systems market, and it is expected to retain its dominance during the forecast period as well. Based on geography, the mortar systems market has been segmented into North America, Europe, Asia Pacific, Middle East & Africa, and South America regions. In addition, in 2022, North America region accounted for a major mortar systems market share; however, Asia Pacific segment is likely to register highest CAGR during the 2022-2030 period.

Mortar Systems Market Analysis: Competitive Landscape and Key Developments

Hirtenberger Defence Systems, General Dynamics Ordnance and Tactical Systems, Thales, Elbit Systems Ltd, Rheinmetall AG, Raytheon Technologies Corporation, RUAG Group, Northrop Grumman Corporation, ST Engineering, Arquus. are a few of the key companies operating as some of the major players operating in the mortar systems market. The market leaders focus on new contracts, product launches, expansion and diversification, and acquisition strategies, which allow them to access prevailing business opportunities.

- In September 2022, the US army awarded an indefinite delivery/indefinite quantity (ID/IQ) contract with a maximum potential value of up to approximately US$ 49 million to Elbit Systems’ subsidiary in the North America region called Elbit Systems America LLC for the supply of 120mm mortar systems.

- In April 2023, the Swiss Federal Office of Armament (armasuisse) signed a contract with GDELS-Mowag worth of US$ 190 million for the production of a second tranche of 16 120 mm Mortar 16 systems. Under the contract, RUAG will supply its 120 mm Cobra recoiling mortar systems.